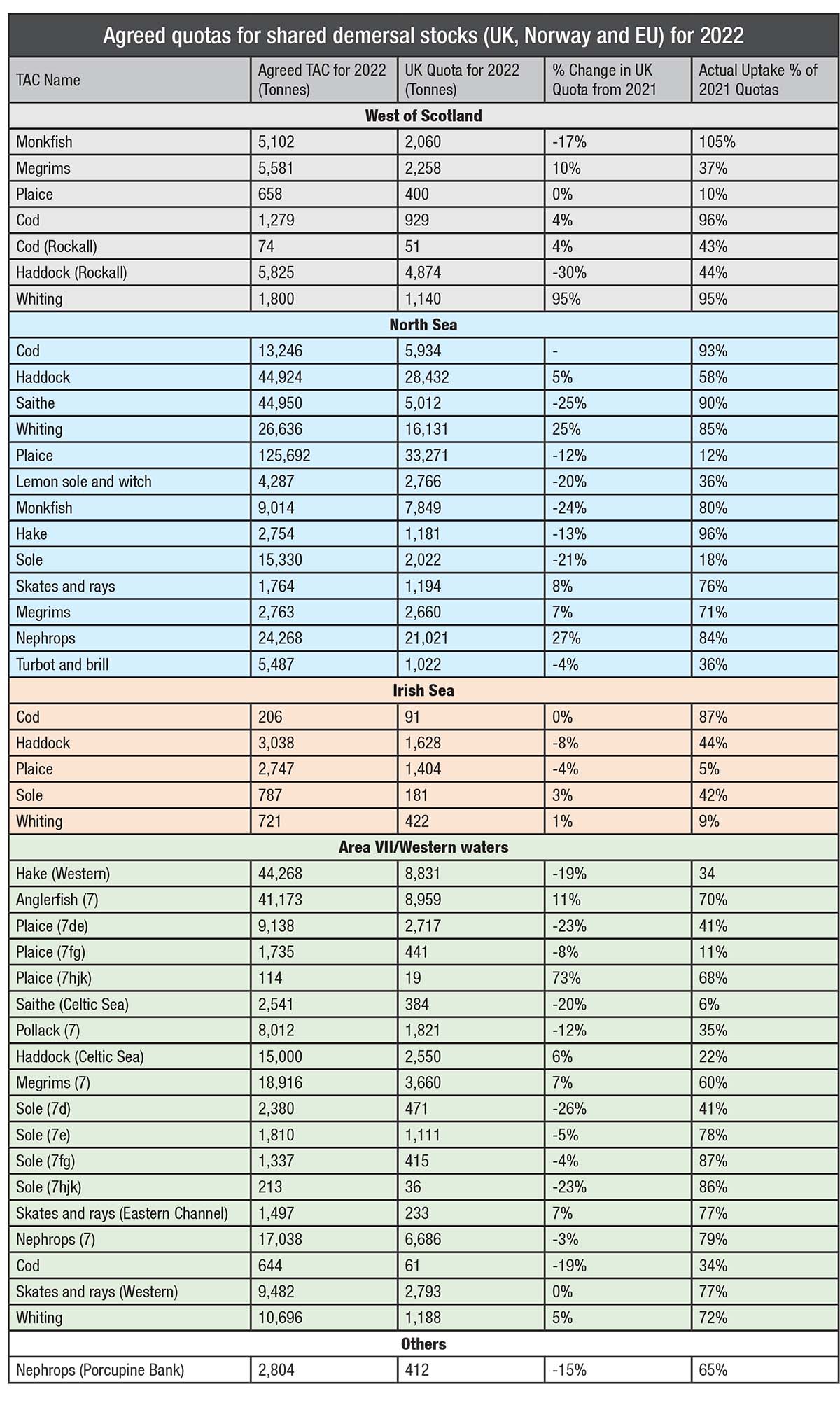

With the usual proviso that these figures are provisional, may not fully reflect international swaps, and in the case of 2021 uptake figures are subject to further revision, the table below outlines the main demersal quotas for 2022.

The uptake percentage figures for 2021 make for sobering reading. A whole variety of reasons can be given for failure to catch what in theory are available and sustainable quotas, based in many cases on full scientific stock assessments.

The Seafish costs and earnings surveys from the year are one pointer – some fisheries, such as the North Sea beam trawl fishery, have been unprofitable, a situation greatly exacerbated by the steep rise in fuel prices seen in 2021. Loss of fishing grounds due to a wide variety of reasons – be it to wind power developments, conservation closures or loss of access to Norwegian waters – is another factor.

Scientists would point to longer-term changes in fish growth patterns and distribution as another alarming, and possibly permanent, change to UK fisheries. Whilst they may not have been able to factor some of this into their own advice and assessments – the huge mismatch between cod availability in the southern North Sea for example, and the north, which are under the same TAC – this may yet have the greatest long-term impact on the industry.

What is clear is that aside from the mixed Scottish demersal fishery, where cod is likely to remain a serious choke species in 2022, and some groundfish species in Western Waters, in the demersal sector at least, quotas are unlikely to be a limiting factor for most of the industry in 2022.

This story was taken from the latest issue of Fishing News. For more up-to-date and in-depth reports on the UK and Irish commercial fishing sector, subscribe to Fishing News here or buy the latest single issue for just £3.30 here.