North Sea and Channel mixed flatfish FMP: a plan, an aspiration, or simple box-ticking?

27th September 2023

Perhaps of all the early Fisheries Management Plans (FMPs) out for consultation, the Southern North Sea and Eastern Channel Mixed Flatfish FMP covers the greatest range of stocks, fisheries and ports, encompassing everything from Anglo-Dutch beamers and Channel fly-shooters landing into the EU to Lowestoft sole drifters and the remnants of the Thames and Channel inshore trawl fleet.

It covers nine different species – lemon sole, witch, turbot, brill, dab, flounder, Atlantic halibut, plaice and sole – several which are treated by ICES as being more than one stock. There is also a mismatch between ICES assessment areas and the areas for the FMP, as well as an overlap between this FMP and that for non-quota species in the English Channel.

EU countries hold significantly bigger proportions of most of the relevant flatfish quotas than does the UK. Further compounding the management challenges, the FMP also embraces six IFCA districts – from the English Channel all the way to the Scottish border with Northumberland – which already have in place measures of their own relating to many of the species concerned.

The Grimsby twin-rigger Jubilee Spirit in Fraserburgh this summer. Where once plaice and other flatfish were an important component of their fishery in the southern North Sea, with catches landed into their home port, Humberside and Yorkshire vessels are now based in North East Scotland for most of the year, as a result of changing fish distribution across the North Sea.

Markets for some of the species within the FMP, such as dab and flounder, are almost entirely in the EU, and catches are for the most part also landed into EU ports, mainly by Anglo- Dutch vessels. The Dutch port of Harlingen is by far the most important landing site for the species within the FMP, with landings in excess of £1m last year. The most important UK port in the ‘fishery’, if it can be called that, is Shoreham, with half the value of Harlingen, and with much of the landings consisting of flatfish bycatch from the large scallopers that work from the port for much of the year, as well as the local fleet of inshore vessels that are based there year-round.

As with the other FMPs currently out for consultation, with a deadline of 1 October, there are a range of summary and supporting documents, although these are much shorter than for some other FMPs – a reflection, possibly, not only of a lack of data about many species which to most fishermen are just a welcome bycatch, but also a lack of ideas about the management of the widespread and very different fisheries that come under this umbrella.

So within the FMP are just five agreed objectives, which can in fact be boiled down to just three: ‘sustainable management’, ‘improved data’ and ‘mitigating climate change’. The consultation recognises that the shallow water of the southern North Sea means that it is susceptible to rapid fluctuations in temperature. This has been reflected in a seismic change in fishing patterns over the last decade as fishermen follow the fish, typically to deeper and cooler waters.

Unlike some of the other FMPs currently out to consultation, detailed proposals and suggestions in this FMP are few and far between.

There are ambitions stated to understand the stocks better, in particular halibut. But whilst the species continues to see a recovery, particularly further north – likely a reflection of overall reductions in fishing effort over the last 15 years – the FMP acknowledges that it is at the southern end of its range, and that halibut caught in the English section of the North Sea are likely ‘wanderers’ that don’t reflect the stock as a whole, and can’t as a result be managed.

A survey for VIId sole is also suggested to better understand stocks, and to feed into the second version of the FMP to be developed in six years’ time.

The only concrete proposal is to introduce minimum landings sizes across the entire area for lemon sole (25cm), turbot (40cm) and brill (35cm). These suggestions clash with a wish stated in the FMP to harmonise MLSs with those already in place within some IFCA districts, where there already is an MLS for turbot and brill of 30cm.

Netting for sole remains a vital part of the income for many inshore fishermen on both sides of the Thames estuary, as well as into the English Channel. Once severely restricted by lack of quota, in recent years the under-10 fleet has seen effort drop due to falling sole numbers inshore – most fishermen blame the pulse fishery for this.

So this is essentially a ‘plan about a plan’, with an aim to gain enough knowledge over the next five or so years to be able to develop a data-based plan when the Fisheries Act obliges Defra to go through the whole exercise again.

The consultation and supporting documentation can be found here.

Drop in effort and landings

The backdrop to the mixed flatfish FMP is one of falling catches for nearly all the species involved, even in years when ICES has recommended TAC increases. Many of the

UK fleet on both sides of the Thames, and beyond, blame much of their drop in landings, particularly of sole, on the pulse trawl fishery, against which they campaigned for many years.

Recovery of the inshore sole fishery since pulse trawling ceased has been slow, although signs of catches picking up are now being reported along the coast. Warmer winter temperatures also mean that some inshore netters have been able to extend their season well past late autumn, when previously they would have switched to alternative fisheries.

The largest drop in effort and landings has been seen by the Anglo-Dutch beam sector, where vessels have reported high catch rates, but increased fuel costs have forced many vessels to tie up for much of the year, or convert to fly-shooting or twin-rigging. Further compounding this has been the relocation further north of many Yorkshire/Humberside whitefish vessels in recent years, due to changed fish distributions attributed to warming seas.

For these shared stocks, the recent round of decommissioning in the Dutch fleet, which took out a significant proportion of the beam trawl segment, suggests that further effort reduction will be seen on the key flatfish species contained within the FMP.

Landings of the main flatfish stocks have seen a steady decline over the last decade, a reflection of reduced effort from both inshore and offshore vessels. Sole (blue line, top graph) has seen the sharpest drop, with recommendations for a 61% cut in the TAC for 2024, but turbot and brill (red line, top graph) and plaice (bottom graph) have also seen declines.

All this should auger well for the surviving vessels in the UK fleet. However, also at play are the changing distributions of the stocks due to warming waters. The shallow nature of the southern North Sea means that summer temperatures there have seen significant increases, with plaice stocks shifting markedly towards the deeper water in Scottish and Norwegian parts of the North Sea.

As temperatures continue to rise, these trends can only continue. This may favour recovery of the sole fishery which, in the North Sea at least, has provided the one significant increase in quota opportunities resulting from Brexit. Whether these increases in quota can ever be turned into landings by the shrinking inshore fleet in the region remains to be seen.

The steady declines in southern North Sea catches reflect changing fishing patterns over the last two decades, including the demise of large portions of the inshore fleet reliant on netting for plaice and sole, and a switch by the Anglo-Dutch beam trawl fleet to the Channel fly-shooting fishery. The mismatch between available quota and actual landings has grown every year, with availability of quota now an irrelevance.

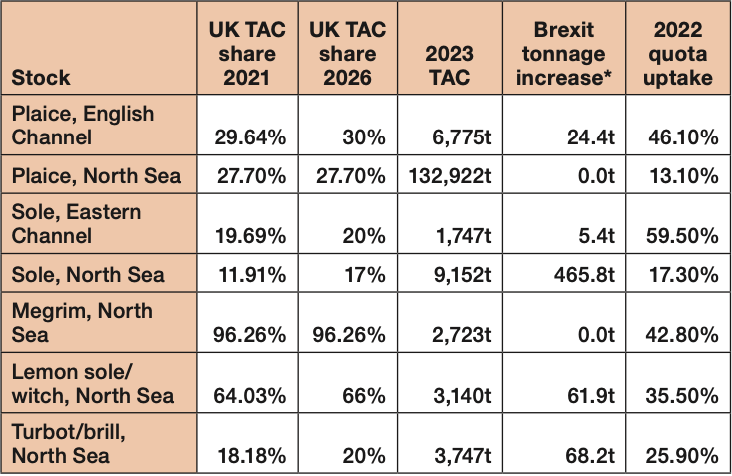

Brexit ‘bonanza’ fails to materialise – but North Sea sole may be the exception

The TCA agreement that followed from Brexit promised quota increases in nearly all the stocks covered in the mixed flatfish FMP. However, for many of these, increases were token, the exception being North Sea sole. A quick glance at the actual figures shows that the quota increases have to date had no impact on fishing activities, with none of the stocks coming anywhere near to being fully utilised. Of the TACs within the FMP, only one, for VIId sole, saw uptake last year above 50% of what was available.

* Applying 2026 share to the 2023 TAC

However, with ICES suggesting that the North Sea sole stock is in trouble, early indications are that advice for 2024 will see a 61% reduction in quota, on top of successive deep cuts in 2022 and 2023 of 28% and 40%. That, FN was told by one Dutch operator, means that a vessel with a 10t annual quota three years ago would have just 1.6t available next year. At that level of cut, and even with the increased share that the UK will receive as part of the TCA in 2024, the quota may yet have an influence on how the fishery is undertaken.

‘Spin and gloss’

June Mummery, managing director of Lowestoft auctioneer BFP Eastern, attended a recent open event hosted by Defra in the port that discussed the FMPs, and the flatfish proposals in particular.

“It’s good they made the effort to come and listen,” she told FN, “but the flatfish FMP is nothing really but spin and gloss, and I said as much to the officials who travelled to Lowestoft.

“The flatfish FMP isn’t really a plan at all, and as far as we are concerned, developing any plan that will help us manage fish stocks will be impossible whilst we have so many foreign vessels in UK waters. There is no mention in the FMP of taking back control to 200nm. We can’t even have exclusive use of 6-12nm.

“A decade after the French, let’s be honest, pushed the Commission to close the pulse fishery, with a bit of help from the small-boat sector of the UK, we are finally starting to see a bit more sole. But it’s taken a decade, and now we see the same flatfish stocks threatened by the wind power industry – not so much the turbines, but the cabling, which scientists increasingly think is having a negative impact on fish stocks.

“I don’t see how we can have an FMP that says it is about managing and looking after stocks, when there is no mention of power cable issues, of pumping out raw sewage onto juvenile flatfish grounds, or of taking back control of our 0-12nm zone. And there is no mention of managing fisheries sustainability, such as limits on horsepower and size of vessels.

“The TCA still sees more EU quota for these stocks than for the UK, and 54% of the UK quota is foreign- owned anyway. If Defra thinks this is management, then the UK fishing industry will never recover, and deprived coastal communities will never rebuild.”

For more up-to-date and in-depth reports on the UK and Irish commercial fishing sector, subscribe to Fishing News here or buy the latest single issue for just £3.30 here.

Sign up for Fishing News’ FREE e-newsletter here.

Main image photo: Geoffrey Lee